Market Scenario

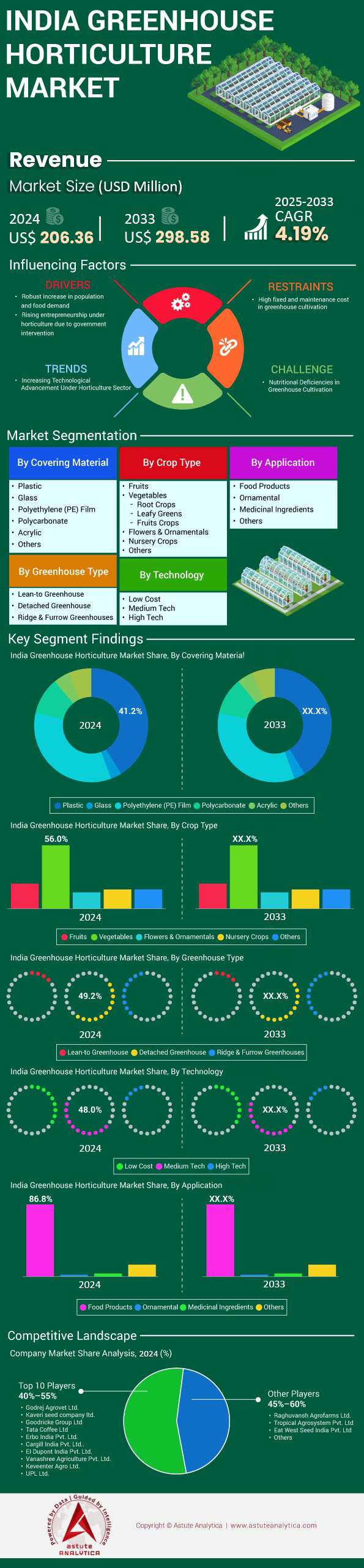

India greenhouse horticulture market size was valued at US$ 206.36 million in 2024 and is projected to hit the market valuation of US$ 298.58 million by 2033 at a CAGR of 4.19% during the forecast period 2025–2033.

Key Findings

- Based on covering material, plastics to remain the largest revenue contributor with more than 41.24% share.

- Based on crop type, vegetables captures the largest 56% market share.

- Based on greenhouse type, the detached greenhouse to account for the highest 49.27% revenue share of the India’s Greenhouse Horticulture market.

- When it comes to technology, medium tech capturing the 48.03% market share.

- Based on application, Food Products to continue leading the market with over 86.86% market share.

A multi-faceted demand structure is rapidly solidifying for the India Greenhouse Horticulture market, propelled by strong economic and policy drivers. Government impetus is creating substantial producer-side pull; for instance, the Mission for Integrated Development of Horticulture (MIDH) has channeled an investment of ₹2,963.91 Crore into protected cultivation. This is complemented by compelling unit economics, where a single greenhouse-grown gerbera flower fetched ₹3.50 in 2024. The tangible prospect of profitability is further evidenced by the projected payback period of 24 to 48 months for a commercial hydroponic farm in 2025, encouraging an influx of new entrants, with 18,500 new farmers expected to benefit from subsidies next year.

Simultaneously, a sophisticated demand from urban consumers is creating new, high-value revenue streams. The explosive growth of the Direct-to-Consumer channel, which attracted USD 757 million in funding during 2024, provides a direct pipeline for premium produce. Urban farms are responding adeptly, with hydroponic systems yielding 7-8 kg of lettuce per square meter every 30 days. The aggregate annual output from greenhouses now stands at 8 million tons, catering to a market that values freshness and traceability. This consumer preference is a powerful force shaping investment in the India Greenhouse Horticulture market.

This domestic demand is augmented by growing international appetite and the requisite infrastructural backbone. In fiscal year 2024, floriculture exports reached 19,678 metric tons, signaling strong global market acceptance. Supporting this growth is an expanding cold chain network, comprising 8,698 units with a capacity of 39.6 million metric tons as of August 2024. This expansion is creating a need for specialized labor, with projections showing 15,000 new skilled jobs by the end of 2025. The sale of 25,000 tons of specialized greenhouse film in 2024 serves as a leading indicator of new construction, directly reflecting this comprehensive demand.

To Get more Insights, Request A Free Sample

Unlocking New Frontiers in India's Greenhouse Horticulture Market Revolution and Growth

- Renewable Energy Integration for Cost Optimization: A substantial opportunity exists in integrating solar power solutions to operate greenhouses. High energy consumption for climate control is a major operational cost. By adopting solar energy, growers can significantly reduce electricity expenses, thereby improving net margins and enhancing the sustainability of their operations. Government schemes promoting solar pumps and rooftop solar provide financial incentives, making the transition economically viable and aligning with India's national renewable energy goals.

- Cultivation of High-Value Nutraceutical and Exotic Crops: There is a growing opportunity in shifting production towards high-value niche crops in the India’s greenhouse horticulture market. Cultivating exotic fruits like blueberries and strawberries, or medicinal plants like saffron and ashwagandha, inside controlled environments caters to premium domestic and export markets. These crops command significantly higher prices per square meter compared to traditional vegetables. This pivot allows growers to tap into the burgeoning wellness and gourmet food industries, securing much higher returns on their investment.

Organized Retail and Quick Commerce Fueling Structured Produce Demand

A powerful demand driver for the India Greenhouse Horticulture market is the rapid expansion of organized retail and quick commerce. These modern trade channels require a consistent, year-round supply of high-quality, graded produce that traditional agriculture struggles to provide. The number of dark stores in India is projected to reach 1,500 by the end of 2025. Consequently, quick commerce platforms now require a minimum daily supply commitment of 500 kilograms per vegetable SKU from partner farms. This creates a structured and predictable demand environment, ideal for greenhouse operators who can guarantee output and quality.

The scale of this demand is substantial and growing across the India greenhouse horticulture market. Wherein, average daily orders for fresh produce on a leading quick commerce platform surpassed 300,000 in major cities in 2024. To manage this volume, the top five players established 250 new farmer collection centers last year. Their investment in supportive cold-chain logistics exceeded ₹250 crores in 2024. Leading retail chains issued supply contracts for over 80,000 metric tons of sorted vegetables. The high rejection rate for open-field produce, at 18% in 2024, further solidifies the preference for superior greenhouse products. The number of active monthly users on these apps surpassed 40 million, expanding into 35 Tier-2 cities in 2025, signaling a deep and widening market.

HoReCa Sector's Gourmet Requirements Creating a Premium Niche Market

The booming HoReCa (Hotels, Restaurants, Catering) sector is creating a highly lucrative niche demand for the India Greenhouse Horticulture market. This industry's focus on gourmet and exotic cuisine necessitates a reliable supply of specialty ingredients that are often delicate and require controlled growing conditions. In 2024, the number of new fine-dining restaurants that opened in India's top eight cities was 210. Furthermore, major 5-star hotel chains collectively sourced an impressive 1,200 metric tons of exotic vegetables last year, showcasing the volume required at the premium end of the market.

This specialized demand translates into very high price points and consistent orders. For example, the average procurement price for edible flowers by premium caterers reached ₹2,500 per kilogram in 2025. The annual demand for microgreens from the Mumbai HoReCa sector alone in the India greenhouse horticulture market was estimated at 60 metric tons in 2024. A single 5-star hotel kitchen places an average weekly order of 75 kilograms for cherry tomatoes. This trend is supported by a growing ecosystem, with the number of food-tech platforms supplying the HoReCa sector growing to 150. The number of cloud kitchens crossed 25,000 in 2025, and with the Food Service market set to employ over 10 million people, this specialized demand will only intensify.

Segmental Analysis

Plastic Covering Materials Assert Market Dominance Through Economic Viability

A granular analysis of covering materials reveals that plastics command the largest revenue share, contributing more than 41.24% to the segment. This market leadership is attributable to the material's superior cost-effectiveness and operational versatility over alternatives like glass. The industry standard involves advanced 5 to 7-layer co-extruded films, typically with a 200-micron thickness, which offer an optimal blend of durability and light transmission. Furthermore, significant government initiatives have been a primary catalyst for adoption. Subsidies under programs like the Mission for Integrated Development of Horticulture (MIDH) can offset up to 60% of the initial polyhouse investment. Since 2014-15, MIDH has facilitated protected cultivation across 2.51 lakh hectares through an investment of INR 2,963.91 Crore.

- Modern greenhouse films incorporate specialized anti-drip and anti-dust technologies.

- The physical barrier created by plastic coverings curtails pest infestation effectively.

- Specialized films provide thermal stability, trapping heat to maintain optimal temperatures.

Consequently, the application of plastic films delivers substantial resource efficiencies, a key driver within the India Greenhouse Horticulture market. These materials can reduce water consumption by up to 60% and concurrently lower pesticide requirements by 40%. The resulting controlled environment also serves as a significant productivity accelerant, boosting tomato yields by 3 to 4 times compared to open-field cultivation. Government support extends to ancillary applications, with plastic mulching subsidized at a rate of up to INR 12,800 per acre. With a typical UV protection lifespan of 3 years, these films offer a compelling return on investment, cementing their foundational role in the market.

High-Value Vegetables Command the Greenhouse Crop Production Landscape in India Greenhouse Horticulture Market

Vegetables decisively lead the crop-type segment, capturing a substantial 56% market share. This dominance is propelled by strong, year-round consumer demand for high-quality, fresh, and off-season produce, which fetches premium prices for cultivators. Protected cultivation environments enable farmers to meet this demand consistently, thereby stabilizing their income streams. Government bodies, including the National Horticulture Board (NHB), actively promote the cultivation of high-value vegetables like capsicum and cucumber through targeted schemes. The total output from this segment is significant, with annual greenhouse vegetable production in India reaching approximately 8 million tons. The economic model is highly attractive, evidenced by a short payback period of just 2 to 4 years for a commercial polyhouse.

- Farmers adopting protected cultivation for vegetables report an average profit increase of 250%.

- The controlled environment allows for tomato harvesting for nearly 8 months annually.

- Greenhouse-grown vegetables meet stringent quality standards for lucrative export markets.

The segment's profitability is directly linked to massive yield improvements, which are a cornerstone of the India Greenhouse Horticulture market. For example, tomato yields can reach 100 tons per acre under protection. Institutional support for scaling up is robust, with the established cost norm for a commercial project reaching as high as INR 112 lakhs. The MIDH scheme provides crucial assistance to individual farmers for a maximum area of 4 hectares. This framework encourages the cultivation of over 40 different commercial vegetable crops, catering to a wide spectrum of market demands. Future projections indicate sustained growth, with leafy greens production alone expected to hit 6.9 million tons by 2030, reinforcing the strategic importance of the market.

Detached Greenhouses Emerge as the Leading Structural Market Solution

An examination of greenhouse types shows that detached structures account for the highest revenue share of 49.27% in the India’s greenhouse horticulture market. The widespread adoption of this model is due to its intrinsic flexibility, relative affordability, and modular scalability, which perfectly aligns with the needs of India's small and medium-sized farmers. Detached units facilitate superior climate control for a single crop type and can be expanded incrementally as an enterprise grows. Government subsidy frameworks are often tailored for these structures, with assistance typically capped at an area of 4000 square meters per beneficiary. Moreover, the National Horticulture Board sets the minimum eligible project area at 2500 square meters, a size ideally suited for a detached greenhouse operation.

- In the North East Region, subsidy eligibility starts at 1000 square meters.

- Support for ancillary water harvesting tanks is provided at INR 100 per cubic meter.

- The Quonset, or hoop house, is a prevalent and cost-effective detached design.

The economic case for detached structures is a powerful driver of their market penetration. Well-defined cost norms for construction stand at INR 844 per square meter for a naturally ventilated tubular structure, with a 15% increase to INR 970 in hilly regions. More economical versions include simple polyhouses at INR 450 per square meter and wooden structures at INR 540 per square meter. Financial support is significant, with credit-linked back-ended subsidies available up to USD 56.00 lakh per project. Market data indicates that commercial viability peaks in units sized between 501 to 1000 square meters, making them a strategic entry point into the India Greenhouse Horticulture market. Such accessibility solidifies the detached greenhouse's position in the market.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Medium-Tech Solutions Strike an Optimal Balance for Agricultural Modernization

Within the technology segment, medium-tech solutions have secured the largest market share of 48.03% in the greenhouse horticulture market by providing a pragmatic and impactful modernization pathway. This tier offers an effective compromise between the high capital outlay of high-tech systems and the limited control of low-tech alternatives. It integrates semi-automated systems for vital functions like irrigation and climate management, which are both accessible and transformative. For instance, the implementation of medium-tech drip irrigation can reduce water consumption by a remarkable 70%. In addition, the use of automated fertigation systems can achieve fertilizer savings of up to 30%, directly enhancing operational margins for stakeholders in the India Greenhouse Horticulture market.

- The typical capital investment for a medium-tech greenhouse ranges from INR 750-1500 per square meter.

- IoT sensor integration for real-time climate and soil monitoring is a key feature.

- Enhanced environmental control leads to a quantifiable reduction in overall crop losses.

The uptake of medium-tech is further propelled by government backing and its proven effect on farm productivity. Initiatives like the Sub-Mission on Agricultural Mechanization streamline equipment procurement, with nominal application fees as low as INR 5,000. Specific components, such as Fan and Pad cooling systems, have an established subsidy cost norm of INR 1400 per square meter. The deployment of these technologies reduces manual labor costs by up to 10% while concurrently improving pest control. Ultimately, these systems are instrumental in elevating farm output by 2 to 3 times over conventional methods, offering a clear return on investment for the growing India Greenhouse Horticulture market.

To Understand More About this Research: Request A Free Sample

Strategic Investments Reshaping India's High-Tech Agriculture Landscape

- Eeki Foods Secures Major Funding (July 2025): The climate-resilient aeroponics startup Eeki Foods successfully raised USD 7 million in a funding round led by consumer-focused venture capital firm Sixth Sense Ventures. This capital is earmarked for expanding their innovative farming operations across India and enhancing research and development.

- BioPrime Agrisolutions Raises Series A (October 2024): Agri-biotech startup BioPrime secured USD 6 million in its Series A funding round. The round was led by Belgium-based impact fund Edaphon, with continued participation from existing investors Omnivore and Inflexor, signaling strong international interest in Indian agritech.

- Fasal Concludes New Funding Round (December 2024): Precision horticulture startup Fasal raised an undisclosed amount from Beyond Capital Ventures. These funds are designated for expanding domestic and international operations and diversifying into new business streams like SaaS intelligence and secondary processing of farm produce.

- GoPurple Obtains Pre-Seed Capital (September 2024): Ahmedabad-based GoPurple, an agritech startup specializing in Fogponics, secured USD 180,000 in pre-seed funding. The investment in the India greenhouse horticulture market will be used to launch their flagship indoor farm and R&D center to advance soilless farming technology.

- Omnivore Fund III Makes Strategic Investments (2024): Venture capital firm Omnivore, through its Agritech & Climate Sustainability Fund III, made several key investments in 2024. These include funding for Agrizy, Bioprime Agrisolutions, and Niqo Robotics (TartanSense), reinforcing its focus on technology-driven agricultural solutions.

- Fasal's Successful Series A Round (January 2024): Kicking off the year, Fasal, a full-stack precision farming platform, raised USD 12 million in its Series A funding round. The round was co-led by TDK Ventures and British International Investment, aimed at scaling its IoT-crop intelligence technology.

- Proparco Invests in Omnivore Fund III (June 2024): Proparco, the private sector financing arm of Agence Française de Développement (AFD), invested USD 5 million in Omnivore Fund III. This investment supports startups developing breakthrough solutions in precision agriculture, B2B marketplaces, and post-harvest technologies.

- Jai Kisan Acquires NBFC License (2024): Agritech neobank Jai Kisan obtained a non-banking finance company (NBFC) license after acquiring a majority stake in supply chain financing company Kushal Finnovation Capital. This strategic move enhances its ability to provide financial services to farmers.

- Fragaria Launches with Pre-Seed Funding (2024): High-tech berry cultivation platform Fragaria was founded in 2024 and secured initial funding to develop its controlled-environment agriculture model. The startup combines hydroponics and precision climate control to grow premium berries year-round under its “Oh! Fruits” brand.

- Kryzen Biotech on Shark Tank India (2024): Kryzen Biotech, a specialist in commercial hydroponic farm setups, gained significant visibility and investment offers after appearing on Shark Tank India Season 3. The company secured offers for both equity funding and joint venture development, highlighting growing mainstream interest in hydroponics.

Top Companies in the India Greenhouse Horticulture Market

- Godrej agrovet Ltd.

- UPL Ltd.

- Goodricke Group Ltd.

- Tata Coffee Ltd.

- Kaveri seed company Limited

- Keventer Agro Ltd.

- Raghuvansh Agrofarms Ltd.

- Tropical Agrosystems India Pvt Ltd.

- Vanashree Agriculture Private Limited

- Corteva Agriscience India Pvt Ltd

- East West Seed India Pvt Ltd

- Ebro India Pvt Ltd

- EI Dupont India Pvt Ltd

- Cargill India Pvt Ltd

- Other Prominent Players

Market Segmentation Overview:

By Covering Material

- Plastic

- Glass

- Polyethylene (PE) film

- Polycarbonate

- Acrylic

- Others

By Crop Type

- Fruits

- Vegetables

- Root Crops

- Leafy Greens

- Fruits Crops

- Flowers and Ornamentals

- Nursery Crops

- Others

By Greenhouse Type

- Lean-to greenhouse

- Detached greenhouse

- Ridge and furrow greenhouses

By Technology

- Low cost

- Medium Tech

- High Tech

By Application

- Food products

- Ornamental

- Medicinal ingredients

- Others

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |